Overtime

Mailtime

Good morning,

It’s that special time of the month where you get to let your voice be heard and get my answers to your chart requests and market questions.

We’ve got plenty of good ones today, thanks to everybody who participated.

Let’s see what is on your fellow readers’ minds!

Questions

Can you show some charts of sector leadership ahead of major tops? Have energy, materials, and industrials (all classical cyclicals that are leading YTD) been leaders into sharp or sustained downdrafts?

Great question. We’ve talked a lot about defensive leadership in recent months, but those sectors may not traditionally be thought of as defensive.

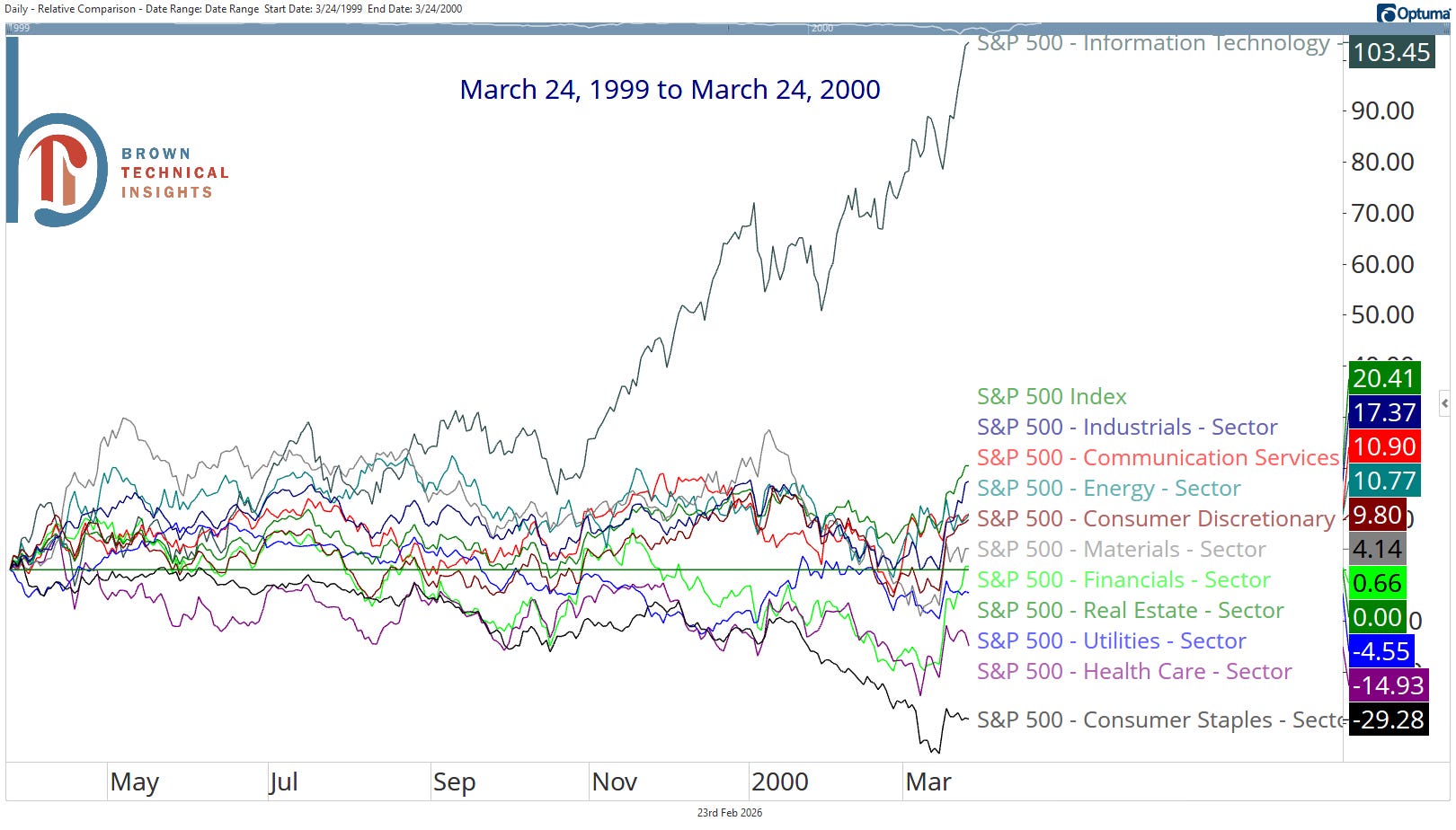

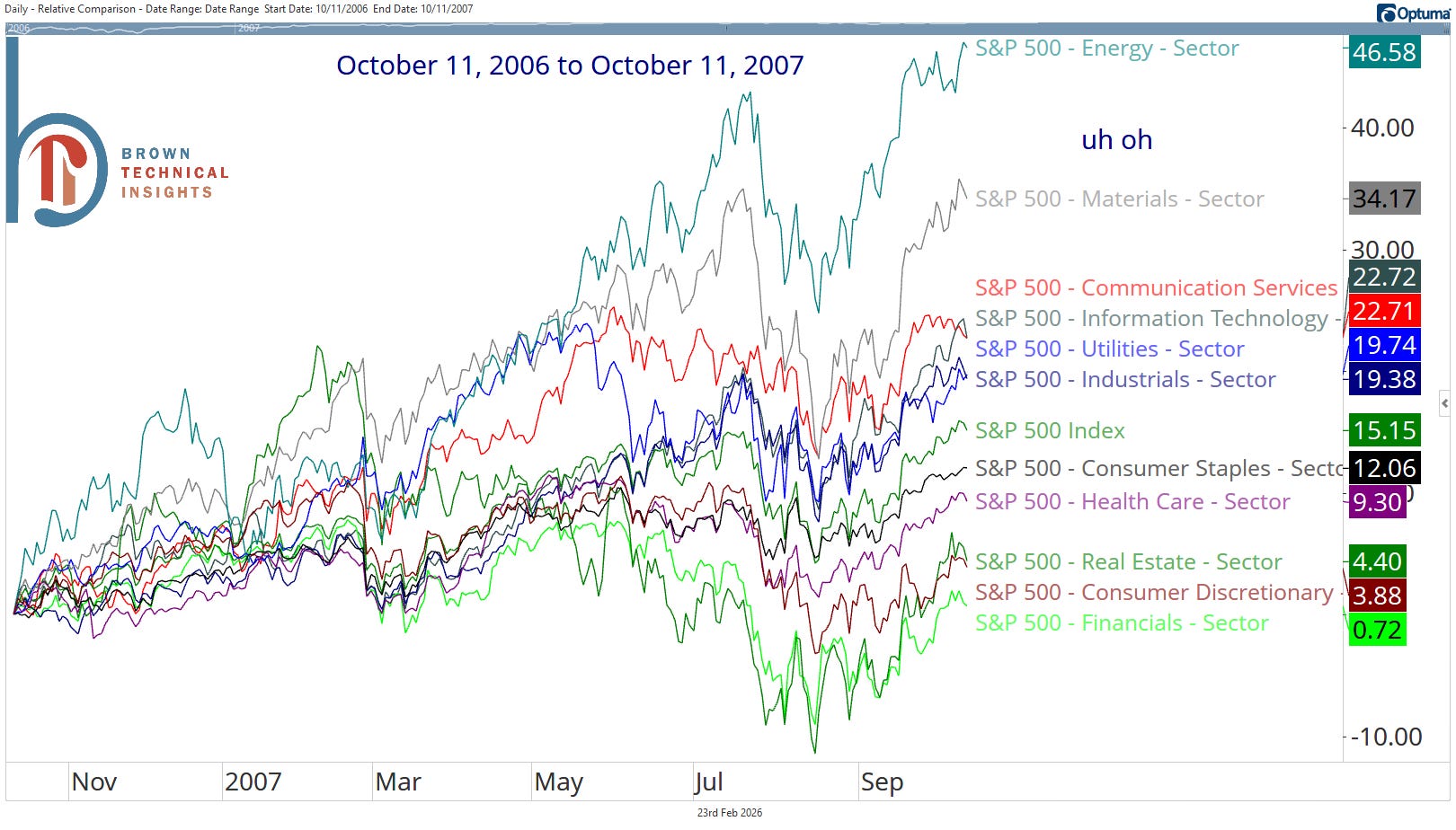

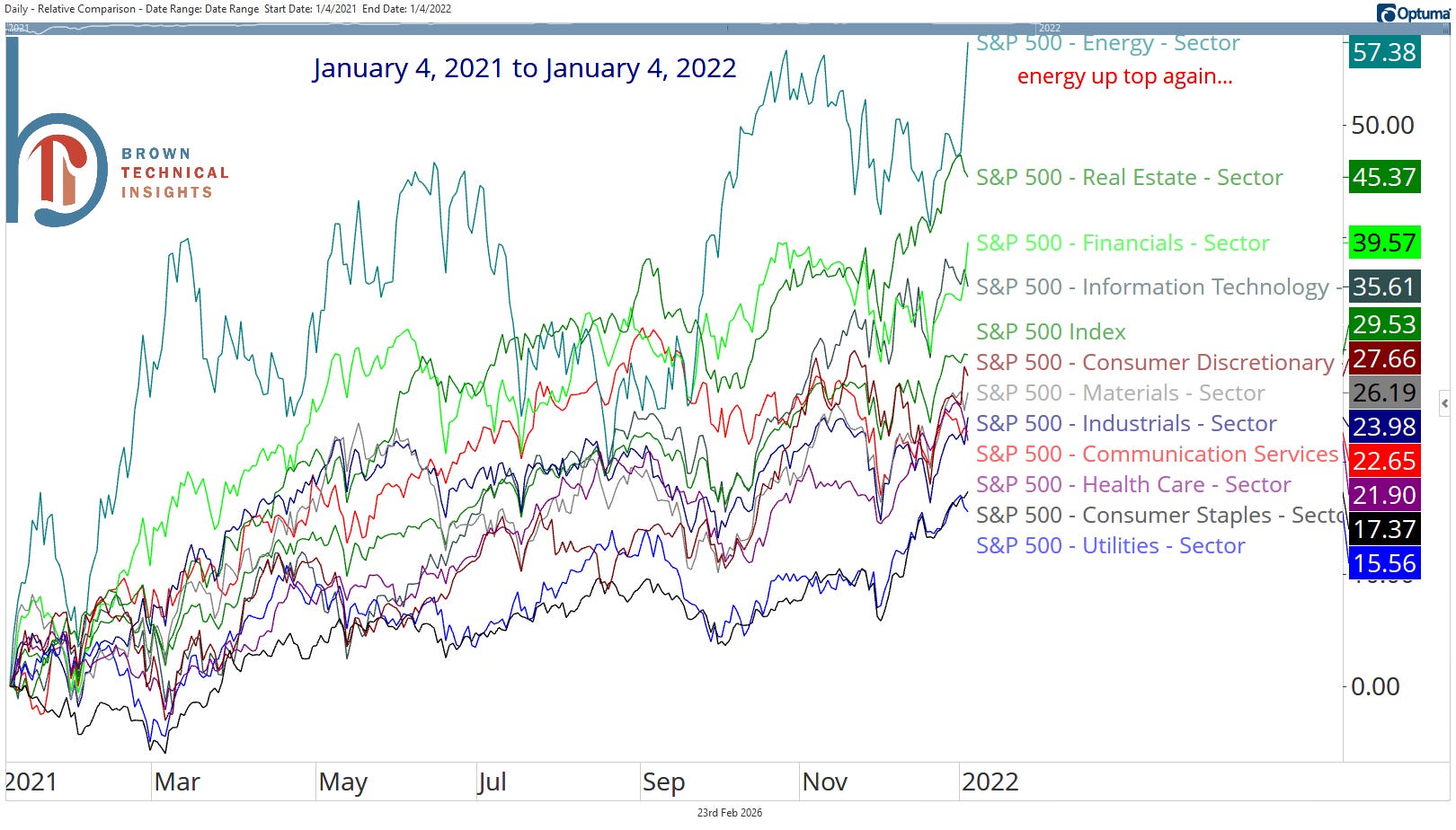

Below are the sector returns for the year ahead of the last three major bear markets. I’m using the dot-com bubble, the GFC, and 2022, and excluding Covid because it came on so suddenly. We also only have S&P 500 GICS sector data back to 1990, so that’s why we’re focusing on more recent history.

As you can see, in two of three instances, energy led into the market top, with materials right on its heels ahead of the Great Financial Crisis.

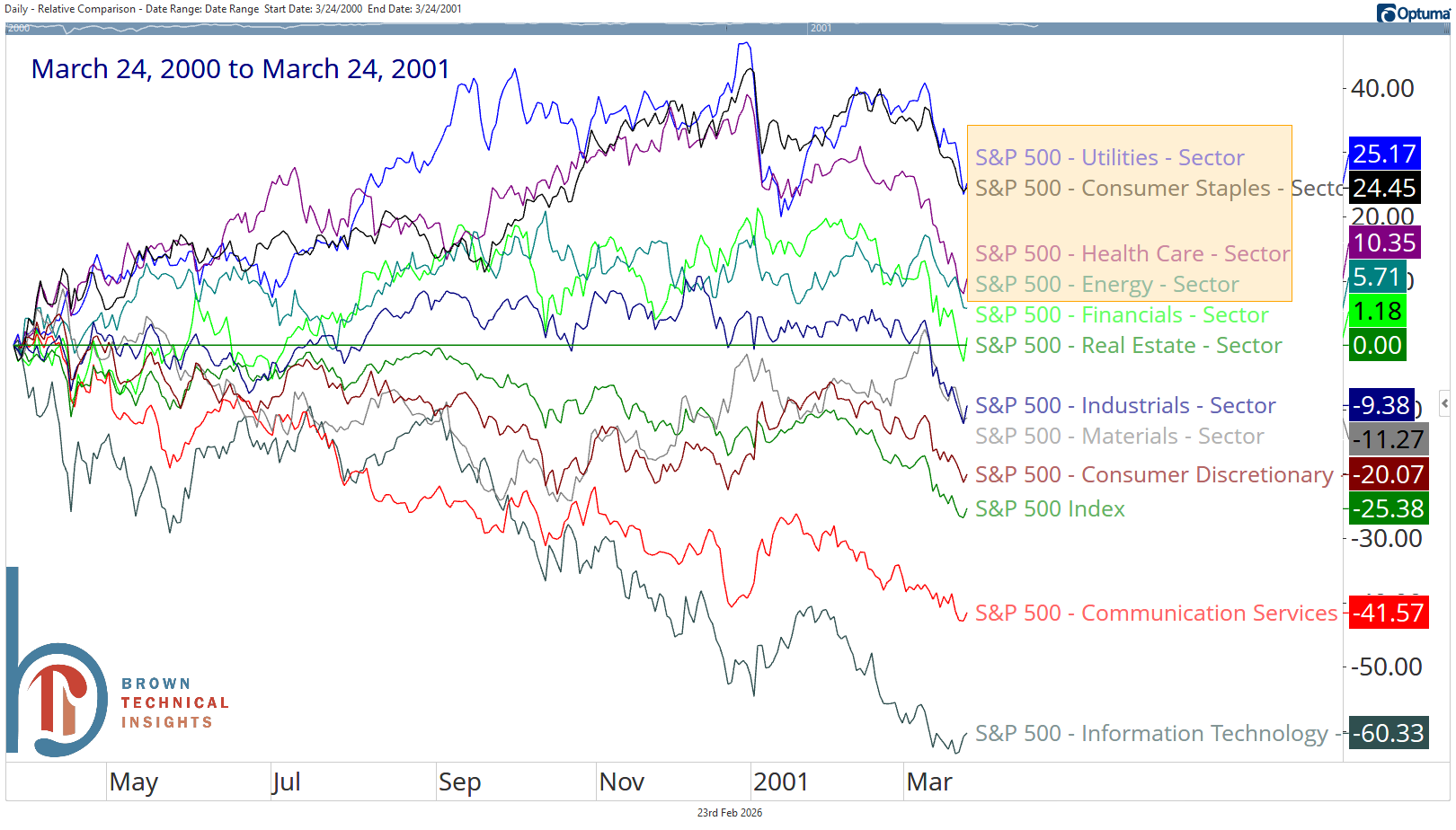

The dot-com bubble is perhaps the exception that proves the rule. The issue with the tech bubble was a breadth one, as you can see almost every sector besides tech declining in the six months ahead of the top. However, I would note that in the year following the market top, you saw classic defensive leadership, and energy positive (+5.7%), and in the number 4 spot:

Unfortunately, all of this lines up with what longer-term studies of history and the textbooks will tell us.

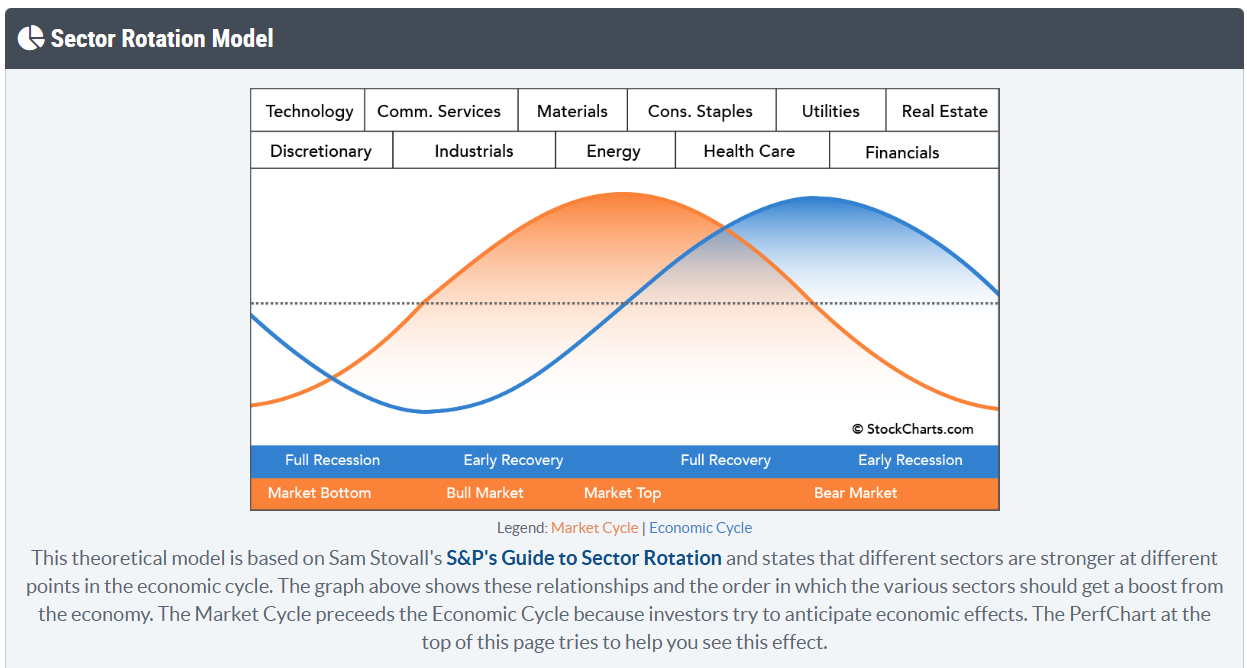

Below is Sam Stovall’s S&P Guide to Sector Rotation, courtesy of StockCharts.com.

The graph shows industrials, materials, and energy as the last sectors to lead at a market top, then, as the top begins, you see the transition to consumer staples, healthcare, and utilities.

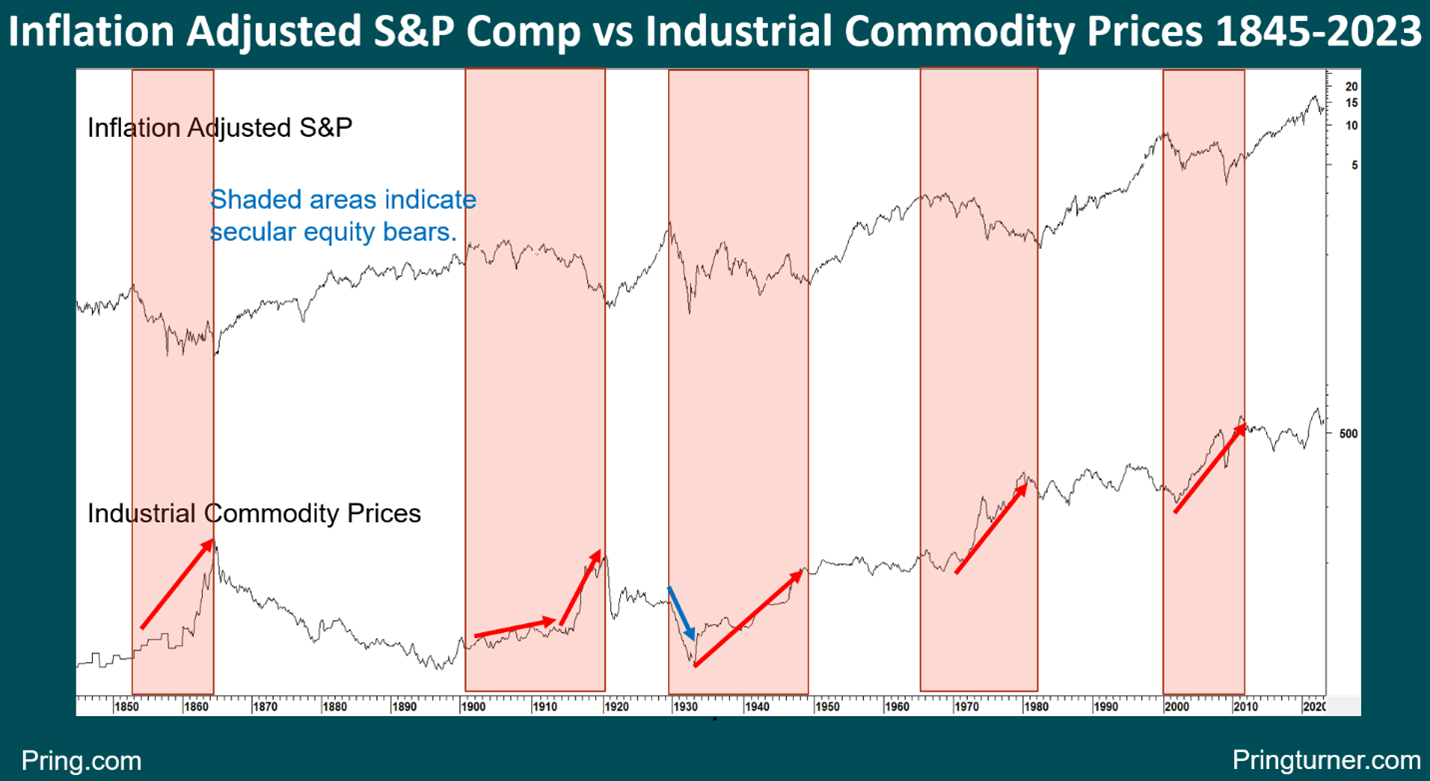

Energy and materials leadership ahead of a market top makes sense when we look at the graph below from Martin Pring:

He shows us that nearly all secular bear markets since 1845 have been associated with sharply rising commodity prices.

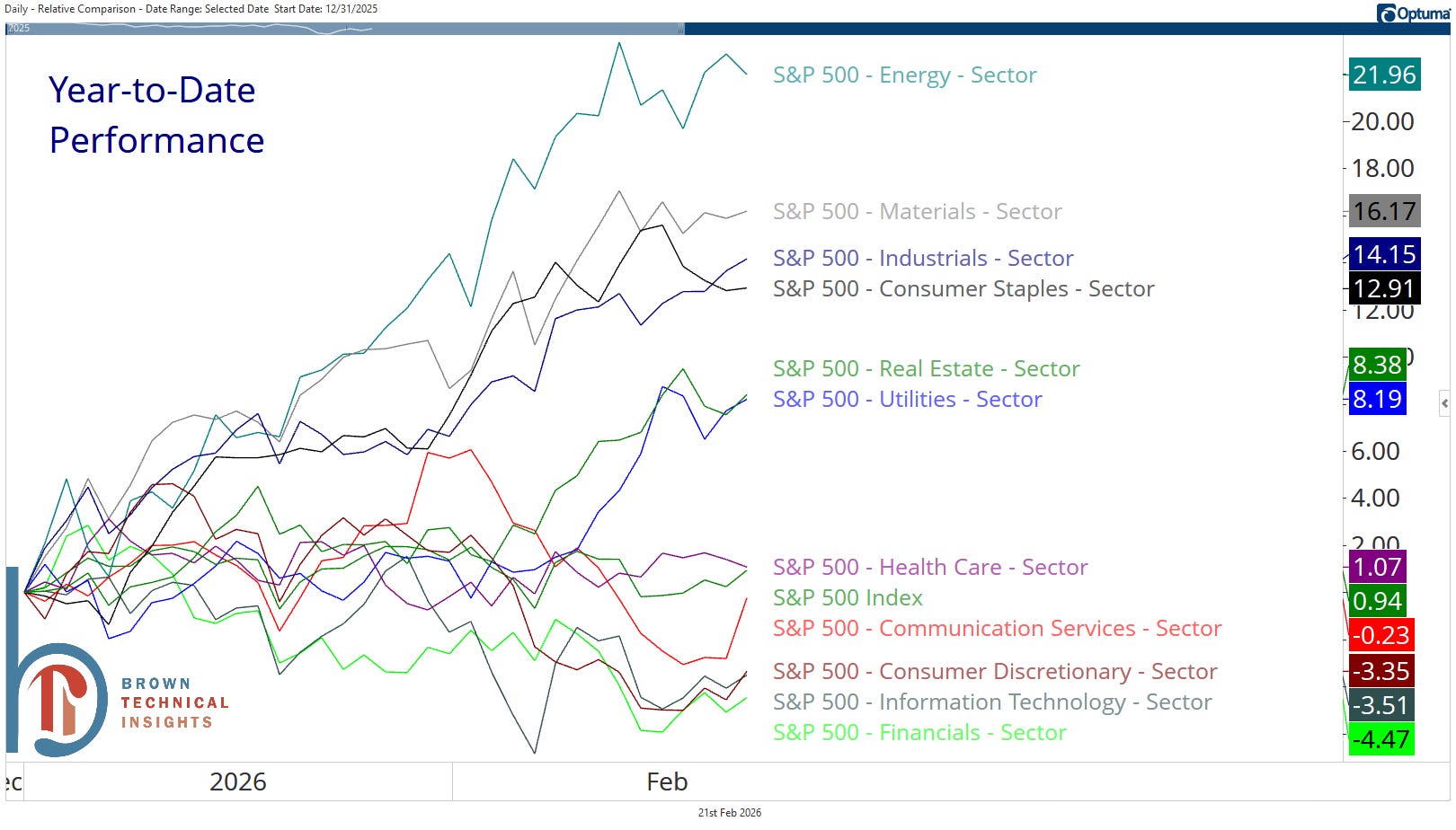

Finally, below is the YTD sector return profile that was featured in yesterday’s Playbook.

Sector leadership isn’t the end all be all. But it’s an important piece of the puzzle and a major reason why I have a more cautious outlook and have been recommending that investors get more defensive.

Chart Requests

AA: Alcoa

Sticking with the commodities and materials theme, Alcoa acts great. It recently completed a multi-year bottom and I see the recent consolidation as a bull flag, likely to resolve higher.