Overtime

Mailtime

Good morning,

Markets are volatile, and the people have questions.

We got some really timely ones this month; thanks to everybody who participated.

Let’s see what is on your fellow readers’ minds!

Questions

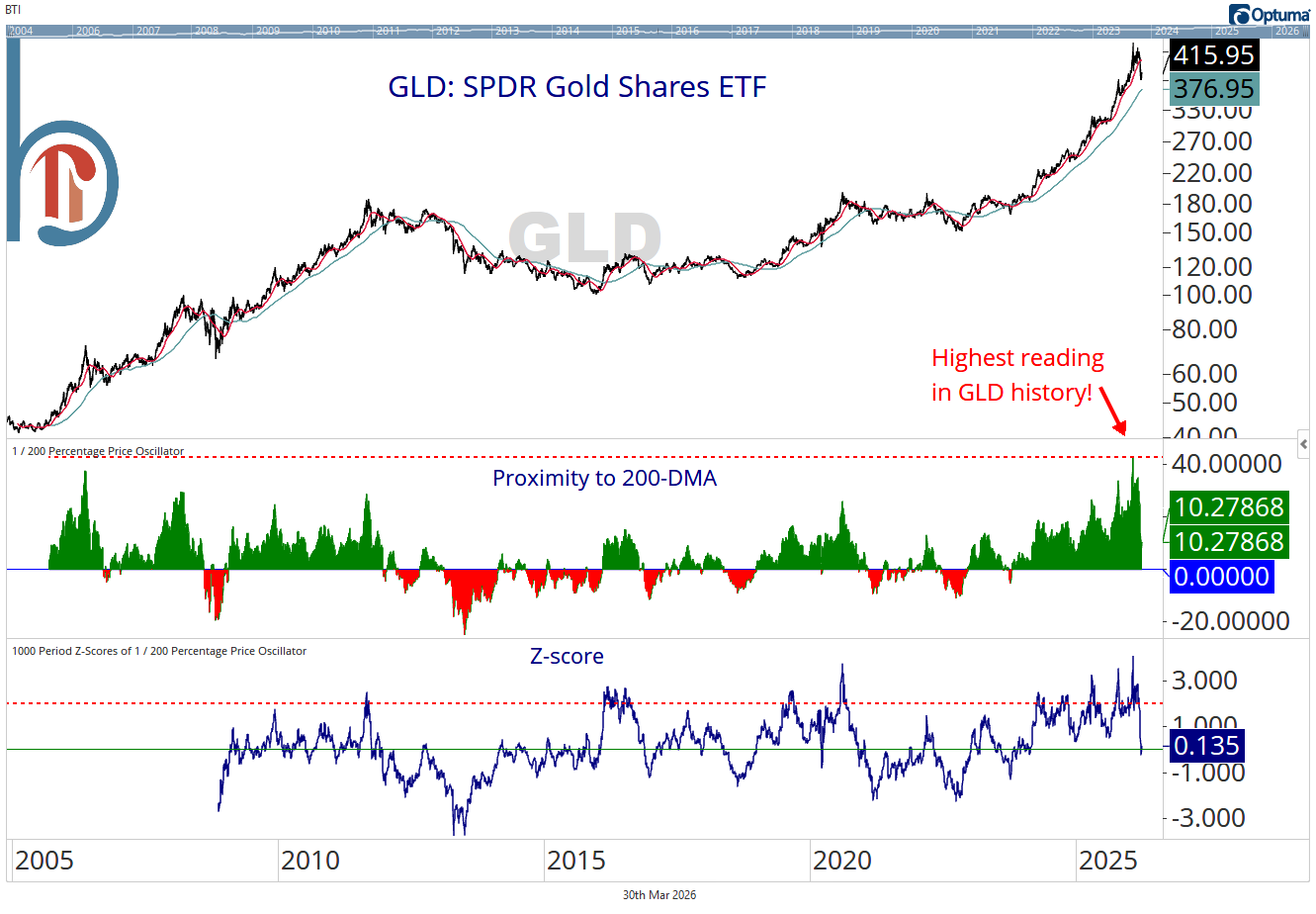

Do you have thoughts on why gold hasn’t held up the last few weeks?

My answer here is nothing more than sentiment. Gold was historically stretched above its 200-DMA, inflows into gold and gold miner ETFs were off the charts, and we saw bearish momentum divergences in GDX at the top. The fact is, it had a huge run, and there were simply no marginal buyers left for gold at the beginning of the month, no matter the news.

Now, much of that has changed in the 30 days since, with GLD seeing the most outflows ever. I think it can bounce, but what that bounce looks like will be telling for the gold trade for the rest of the year. A double-top has been completed, so I’m personally skeptical we will see it get above the 50-DMA (just below $5,000/oz.).

Are there any areas of international equities that are still working?

If by working, we mean immune from recent weakness, then no. The best we can really find is relative strength, and there isn’t a lot of that either, with former leaders like Taiwan forming possible tops.

If you were determined to invest outside the US, one country worth a look would be Canada:

It has fallen below the 50-DMA in absolute terms, but traded to fresh 52-week relative highs vs. SPX yesterday. There’s a clear connection to the energy trade, but the combination of relative strength before the oil/energy spike and recent outperformance is rare right now.

What are your thoughts on reflation vs. stagflation?

Common sense would tell me that stagflation is a bigger risk following an oil supply shock. Inflation is self-evidently higher, and consumers have less discretionary income, a negative for growth.

However, what I find interesting is that market-based inflation expectations aren’t moving up at all. In fact, the five-year, five-year forward rate has fallen since the oil spike, suggesting that the impact to inflation won’t be material, and perhaps even a net negative as slower growth and/or recessions tend to be deflationary.

Can you review the correction checklist?

Absolutely! Our correction checklist is: