Overtime

This vs. That

Good morning,

This week we’re taking a semi-frequent section of The Monday Morning Playbook, called This vs. That, and making an entire report of it.

This vs. That is just what it sounds like, it’s a collection of relative strength or ratio charts showing how an asset class or sector is performing relative to another.

Today’s report will highlight 10 that tell the story of the first half of 2024 and give us some insight into which asset class, sector or area of the market we should be favoring in the second half.

Let’s get into it.

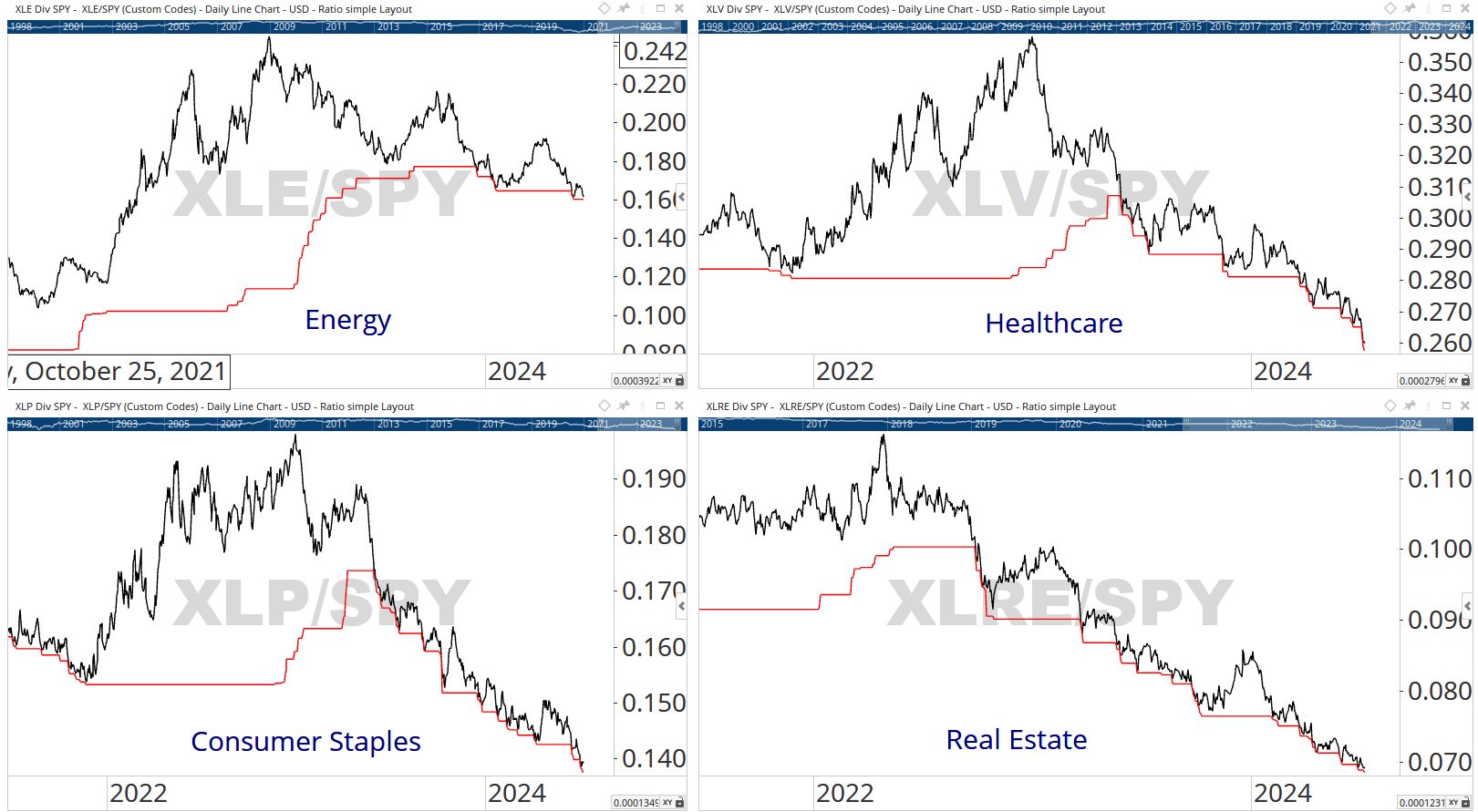

The S&P 500 versus… everything

8 of 11 sectors made a 52-week relative low in June

As shown above, 8 of the 11 S&P 500 sectors made a 52-week relative low vs. the S&P 500 in June. The only sector outside of tech and communication services to not do so was utilities, which traded to 3-month relative lows yesterday.

International equities no better

Broadly speaking, international diversification hasn’t helped, as both EAFE and EM made new all-time relative lows vs. SPX in June. EM has shown some signs of trying to base but both ratios remain below their 1-year moving averages which have been helpful “stay away” indicators over the past decade.

Growth vs. value

The story of 2024: Growth blows it out vs. value

There’s no doubt that one of the most important ratio charts in the first half was growth over value. The Russell 1000 Growth ETF outperformed its Value counterpart by 21% in the first half, which is a lot but actually less than the rolling 6-month outperformance at this time last year. While this ratio could be tactically stretched, it’s important to recognize that this move is coming out of an over 3-year base, suggesting there could be a lot more room to run long term.